The 10 commandments of really successful and confident investing

How you invest your financial assets is key to your financial future. So, it should be at the heart of your financial planning process.

Effective and successful investing doesn’t happen by accident. As with most things, you should always have a plan in place, and follow that when you’re building – and managing – your portfolio.

I strongly believe that you should have some guiding principles that create a framework within which you can make decisions about your investment strategy.

Here are 10 investment “commandments” for you to adopt. These very much reflect my investment ethos and the way I look to advise all my clients when it comes to investing your money.

1. You must have a plan, and stick to it

On your virtual tablets of stone, this commandment is probably the most important.

Your plan will be the result of long and detailed analysis of your circumstances and aims. It’ll become the roadmap that guides all your investment decision-making.

Without a plan you’ll be rudderless and there’ll be little coherence to how you invest.

2. Invest for the long term

If you’re not already investing money, don’t delay. The time to start is now. The sooner you’re in the market, the sooner your money can potentially start to grow in value.

Once you start investing, you should try to keep your money invested for as long as possible. To use an investment cliché, “it’s time in the market, not timing the market”. By that, we mean that the length of time you invest will have a bigger impact on your success than when you buy or sell certain funds or shares.

The two main reasons for this are compounding, and reinvesting dividends.

Compounding

It’s alleged that Einstein described compounding as “the eighth wonder of the world”. In simple terms it means “growth on growth”. So, if you invest £1,000 and it grows by 5% in a year, the next year’s growth is on £1,050 – and so on.

Reinvesting dividends

An extension of compounding comes when you reinvest dividends rather than take them as income. You’re buying more shares or units when you reinvest, so future growth will be based on a larger holding.

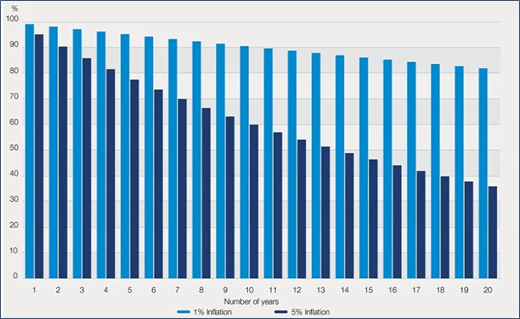

3. Understand that inflation is probably the biggest threat to your future prosperity

Inflation reduces the value of your money in real terms, and so reduces your spending power.

An inflation rate of 5% means that it’ll cost you 5% more to buy goods from one year to the next. Effectively, £1,000 becomes worth only £950.

While you’re working, you can offset the impact of this through salary increases, changing jobs and altering your spending habits. But once you’ve retired, not all those options are available.

I use this chart a lot, because I think it’s very impactful.

You can clearly see that, over an extended period, an inflation rate of 5% can have a devastating effect on the buying power of savings.

Bank of England UK CPI data (Source: Schroders)

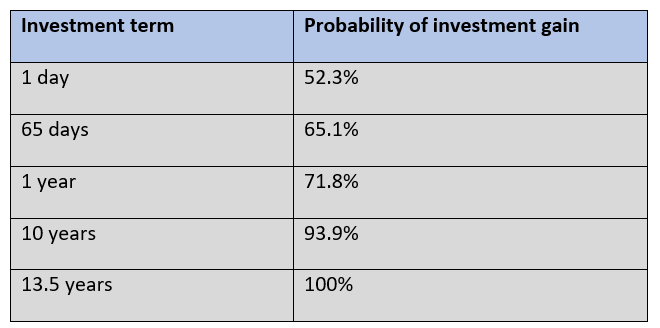

4. Appreciate that investment risk is a good thing

Of all the commandments, this is the one I expect you to struggle with most.

Taken in isolation, it’s easy for the expression “investment risk” to conjure up images of city traders in brightly coloured jackets shouting at each other, and people losing a fortune during a stock market crash.

So let me caveat it for you by saying that investment risk must be managed, and acceptable to your personal outlook and circumstances.

The best mitigant to investment risk is time. Research carried out by Macrobond – the world’s largest macroeconomic and financial database – illustrates this.

By studying investment markets from 1971 to 2020, they produced the following data based on length of investment and chance of investment gain:

Source: Macrobond

The other key factor around risk is accepting investment volatility as your friend rather than something to be feared. Investment guru, Warren Buffet, summed this up nicely when he said “be fearful when others are greedy, and greedy when others are fearful.”

Many people will worry when markets are falling, but the wise investor will see this as an opportunity to buy at a low price, and therefore turn a tidy profit when markets recover.

5. Always diversify your investments

Diversifying your investment portfolio is another effective mitigation against investment risk.

Spreading your money across different asset classes and different markets around the world can help reduce the impact of volatility on your investments’ overall performance.

This is because many different assets tend to be “negatively correlated”, which means they react differently to different market conditions.

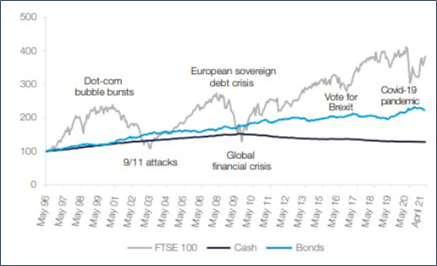

6. Be sure to keep a level head

You shouldn’t be spooked by sudden market falls – they are part and parcel of investing. Likewise, you shouldn’t get carried away if the value of your funds suddenly increases.

Volatility is very much part of investing.

In the immortal words of Corporal Jones from Dad’s Army: “Don’t panic!”

To illustrate this, the chart below shows an investment of £100 in May 1996, and assumes you reinvested all dividends and income, in line with our second commandment.

Over the next 25 years, there were a series of cataclysmic market events during which you may have been sorely tempted to switch into lower-risk investments, or even “cash out” entirely.

Source: Brewin Dolphin / Datastream

But, as you can clearly see, switching to low-risk options like bonds or cash would have cost you a lot of money overall.

7. Be selective about the investment advice you act on

Don’t believe all you read about investments in the media or see online, and take any investment tips with a big pinch of salt.

No one can safely “time” the market. For every person who claims to have made a fortune by predicting a crash or a boom before it happened, there are hundreds – if not thousands – who didn’t.

It’s no secret that the most successful investors follow a simple set of rules. Warren Buffett is an obvious example of this. His process is simple and based on a few core principles, rather than sitting in front of a computer all day hoping to strike lucky with a particular trade.

8. Reduce your stress levels by keeping things simple

The most effective approach to investing – and financial planning in general, for that matter – is usually the simplest.

A portfolio containing a good, diversified mix of stocks and funds can be just as productive as one containing a whole series of complicated financial instruments. Remember, the 2007/08 crash was caused, in part, by financial regulators not understanding the products financial companies were selling. If they didn’t understand them, what chance did the average investor have?

Investing shouldn’t be stressful. If you find yourself worrying about your investments, then something is wrong, and your plan needs to change.

9. Be prepared to ignore your portfolio for extended periods

Don’t check the value of your investments too frequently. You’ll fall victim to the problems we outlined in our 4th commandment.

Overreacting to short-term performance – good or bad – rather than accepting it as a natural outcome of investing money, is one of the worst mistakes you can make.

10. If your circumstances change, then so should your plans

Remember John Maynard Keynes’s famous quote: “When the facts change, I change my mind.”

Although it’s important to have a plan, it’s equally important that you regularly review it and change it if necessary. This is especially true if your personal circumstances change.

Likewise, as you get closer to stopping work, and want to start enjoying the benefits of your investments in the form of retirement income, you’ll want to review your investments and potentially change your plan.

Get in touch

If you want to talk through your own investment plans and find out how I can help you, please give me a call on 07769 156 250.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Foster Denovo Limited is authorised and regulated by the Financial Conduct Authority.

The Financial Conduct Authority does not regulate school fees planning, taxation & Trust advice and Will writing.