10 key financial questions you should be able to answer

Successful personal financial planning can often come down to self-awareness and being prepared to challenge yourself.

Only you will have the detailed insight into your own finances, how you spend money, and what your financial priorities are.

It’s therefore important to be honest with yourself so you can change any bad habits and give yourself the best possible chance of financial success and being able to live comfortably.

Here are ten questions I think you should be able to answer.

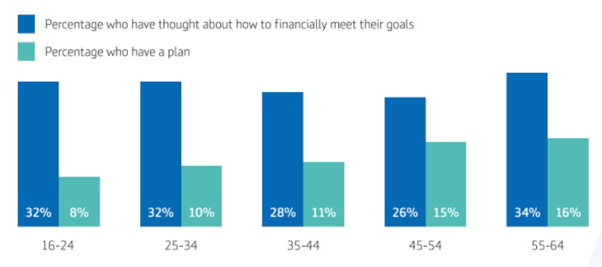

1. Have you got a financial plan?

If you don’t already have a financial plan in place, then putting one together should be one of your key priorities.

A recent study by Aegon found that relatively few people had made a financial plan, something the insurer says is key to “successful financial wellbeing”.

It doesn’t have to be detailed at this stage. You can start with simple spreadsheet that maps your income and expenditure. Then make a note of your assets – including the value of your pension and savings – together with your current debts and liabilities.

Then spend some time setting down with your spouse or partner and talking through your life goals. Having a clearer idea of what you what to do makes it easier to plan your finances to be able to fulfil your aims.

2. What’s your plan to clear your debt?

There are two different types of debt.

“Good debt” is where you’ve borrowed money at a competitive rate of interest to secure something tangible for yourself and your family. A mortgage is the obvious example of “good debt”, a car loan another.

“Bad debt” is unsecured borrowing – mainly credit cards. High interest rates and the impact of compounding mean that it can take ages to pay these off, and therefore reduce your monthly disposable income, if you don’t have a firm plan in place to clear it.

3. Do you spend more than you earn?

Your financial plan will tell you if your outgoings exceed your income each month. If this is the case, then it likely means you’re having to resort to borrowing to bridge the gap each month.

This then creates a snowball effect as the increased cost of borrowing eats into your monthly income.

If you aren’t living within your means now, you’re less likely to be able to do what you want in the future.

4. Are you saving enough for your retirement?

Saving for your retirement should be a big priority.

Pensions are one of the most tax-efficient ways to save money in the long term, especially if you’re a higher-rate taxpayer.

The same compounding that can make credit card debt so difficult to clear can also have a beneficial impact on your pension savings. So, the sooner you start saving and maximising the amount you save, the better.

If you already have pension arrangements, get projections to see how much they will be worth at your planned retirement date. This will give you a good idea if you’re current contributing enough or whether you need to increase the amount you’re saving.

5. How are your savings and your pension fund invested?

If you’re saving money on a regular basis, and already have assets invested, you should make sure it’s invested appropriately.

Making sure your money is working hard can make a big difference to your wealth, and help you cope with any market turbulence that can blow plans off course.

Different criteria can impact on how you invest. These can include what the money is for, the length of time it’s invested for, and your general attitude to investment risk.

6. How much tax do you pay?

You should always have a clear idea of how much tax you pay.

Being aware of this can help you make the right decisions when it comes to where and how you save and invest your money. Some savings and investment schemes are more beneficial than others, depending on your tax status.

It will also encourage you to keep your financial paperwork in order, so you’re able to complete an accurate tax return each year, which will give you more insight into where you can make potential tax savings.

7. Have you got an emergency fund in place?

A “rainy day” fund is one of the simplest, and most obvious, financial necessities, but I’m still surprised at the number of people I speak to who don’t have any immediately accessible savings for use in an emergency.

All you need to do is ask yourself: what would happen in the event of your employer going bust, or if you have a big household emergency? The importance some immediately accessible savings becomes clear.

As a rough rule of thumb, you should have at least three months’ net household income in your emergency fund.

8. Are you planning to move house in near future?

If you have young children, it’s likely that – at some stage – you’ll need to move to a bigger house. Conversely, if your children are older, you may well be thinking of downsizing in the near future.

Both scenarios will impact on your financial position, so it’s worth starting the planning process well in advance, even if it’s just in outline form.

9. What would happen if you are unable to provide for your family?

One of the most important financial steps you can take is to make sure your family will be cared for should you lose your ability to work.

We touched on having an emergency fund above, but you also need to consider the impact of any longer-term financial problems.

Most employers will only continue paying employees who are unable to work for a limited period, and what would the situation be if you run your own company?

10. What if the very worst happens?

Death is obviously an uncomfortable subject to think about, but you owe it to your loved ones to ensure that you’ve plans in place to protect them should the worst happen.

This applies on both a practical and financial level.

Your death will clearly be a stressful time for them, so taking steps to ensure your affairs are up to date, accessible and in order will give them one less thing to worry about at a time of great emotional upheaval.

Also, knowing that they will be financially comfortable will be reassuring to both you, and them.

Get in touch

Taking time to consider these questions, and trying to answer them, can be a key step to ensuring you have robust financial plans in place to deal with emergencies, and plan for your future.

To find out more please give me a call on 07769 156 250.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Foster Denovo Limited is authorised and regulated by the Financial Conduct Authority.

The Financial Conduct Authority does not regulate taxation & Trust advice and Will writing.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.