When it comes to investing, all that glitters isn’t gold

In a crisis, people flock to safe assets. Volatility in the stock market in 2020 might have made you consider fleeing to the relative safety of cash (although I have already talked about why it’s important to keep calm during uncertain periods).

Of course, putting your money in cash right now is also a risk. Although your capital may be secure, interest rates on savings products are at record lows, so there’s a strong chance your money won’t even keep up with inflation. According to Moneyfacts, the average interest rate on an easy access savings account in July 2020 was just 0.4%, whereas the rate of inflation was 1.5%.

So, is there a safe asset from which you can generate a return? In times like these, many investors look to gold thinking that it will ‘save’ them from the decline in the value of their portfolio. The value of gold recently reached an all-time high, however, it’s actually a highly speculative asset that rarely produces anything.

Here’s why the streets of profit are rarely paved with gold.

Gold isn’t really an investment

Gold is an inert metal. It produces nothing, yields nothing, and its value exists only by common consent.

BP produces oil and refines petrol and diesel for the market. Apple produces consumer electronics that are in high demand. AstraZeneca produces highly effective drugs and other remedies.

Companies produce things of value. This means an investment in a sound company should grow over time. The company’s assets, earning potential and actual earnings are likely to be growing. Additionally, if the company you invest in is paying dividends, those dividends should increase as the company grows.

Compare this to gold. Gold has no intrinsic value, produces nothing, and generates no income. Any return on gold is based entirely on price appreciation.

As investing titan Warren Buffett says: “The problem with commodities is that you are betting on what someone else would pay for them in six months.

“The commodity itself isn’t going to do anything for you….it is an entirely different game to buy a lump of something and hope that somebody else pays you more for that lump two years from now than it is to buy something that you expect to produce income for you over time.”

And, if you buy actual gold, it costs you a lot of money when it comes to storage and insurance. Buffett adds: “It’s a lot better to have a goose that keeps laying eggs than a goose that just sits there and eats insurance and storage and a few things like that.”

Stocks and shares outperform gold over time

Even though the price of gold hit an all-time high of more than $2,000 in August, it has still underperformed shares.

Gold’s previous all-time high (of $1,850) was in August 2011 at the height of the global financial crisis. The day the price of gold reached $1,850 (11 August 2011), the S&P 500 index closed at 1,173. When it reached its high of $2,031 on 7 August 2020, the S&P 500 index closed at 3,349.

So, over the best part of a decade, gold’s value only increased by around 7%. In contrast, the S&P 500 index rose by around 185%.

Let’s go back even further.

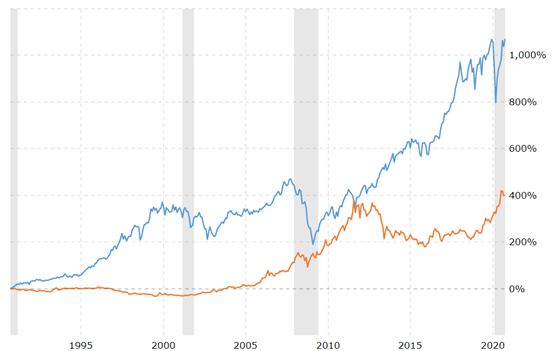

Here’s a comparison between the price of gold (orange) and the Dow Jones Industrial Average index, between 1990 and 2020.

Source: Macrotrends

The chart shows the price of gold increased by around 400% over the 30-year period, whereas the Dow Jones rose by more than 1,000%.

The New York Times has published data which highlights the underperformance of gold over an even longer period.

The economists Robert Barro and Sanjay Misra reported that, from 1836 to 2011, gold earned an average annual inflation-adjusted return of 1.1%. In contrast, they estimated long-term returns to be 1% for Treasury bills, 2.9% for long-term bonds, and 7.4% for shares.

There’s also an over-supply of gold

We’ve seen that gold doesn’t generate an income, has no intrinsic value, and generally underperforms stocks and shares in the long term.

Additionally, the uses for gold (jewellery, decoration) pale in comparison to the supply of gold. The supply of gold outstrips the demand.

Commodities such as wheat, barley, oil, and gas have significant uses that can meet – or even exceed – supply. It’s the demand for these commodities that ultimately determines their price.

So, although the price of gold is influenced by some supply and demand elements, gold is nothing like other commodities.

Gold might seem like a safe haven, however, it offers very little in terms of a long-term financial plan. In many ways, it’s just a speculative asset that never produces anything.

Get in touch

To find out how I can help you to put a robust financial plan in place, so you achieve your future aspirations, please give me a call on 07769 156 250.

Foster Denovo Limited is authorised and regulated by the Financial Conduct Authority.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.