Why tax planning becomes more important after you’ve retired

A key part of my role as a financial planner is implementing the necessary measures to help you enjoy financial security in retirement.

In the years before you retire, a key part of this involves tax planning, including using tax allowances and minimising your liability whenever possible.

However, that’s only half of the job, because it’s important that the planning doesn’t stop when you are no longer working.

In fact, I’d say that tax planning is even more important after retirement than while you are working.

Here’s why.

You are likely to have income from different sources

During your working years, it’s likely that your income arrangements will be relatively straightforward, involving a primary monthly income from your employer or business that is taxed as PAYE.

But when you retire, your income may well be derived from several different sources, each of which may be taxed differently.

These may include:

- Your State Pension

- Income from investments

- Company and personal pensions

- Savings you have accrued

- Dividend income.

Furthermore, you may have rental income from a property portfolio, which can add an extra layer of complexity.

Without an effective and sustainable strategy that looks to provide you with a tax-efficient income from the various sources available to you, it is easy to end up paying too much tax.

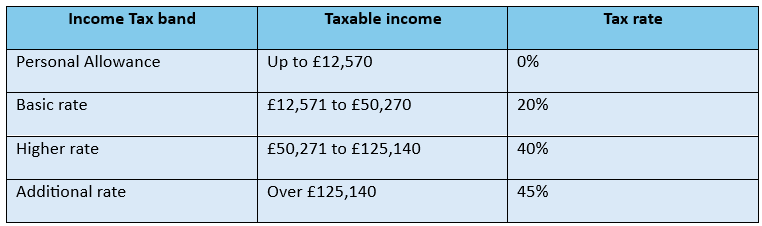

You need to make use of all available allowances

An important part of your retirement income strategy is to make full use of all the tax allowances available to you.

You should bear in mind that allowances are also available to your spouse or partner, so there may be opportunities to create a joint income with both of you maximising your allowances.

For example, as you can see from the table, you both have a Personal Allowance for the 2026/27 tax year of £12,570, which means that you can draw a combined income of over £25,000 without paying Income Tax.

Similarly, you both have an Annual Exempt Amount of £3,000 for Capital Gains Tax, as well as other allowances for savings and dividend income, which are subject to your marginal rate of Income Tax.

All of these allowances can help reduce the tax you pay on investment income.

It’s also worth being aware of the income at which you start paying Income Tax at 40% and factoring this into your tax planning.

An overarching plan that ensures you take income from different sources and maximise allowances can minimise your overall tax liability.

Creating a tax-efficient retirement income from your pension fund

The bulk of your income will probably come from pension funds, so your tax planning arrangements must take into account how and when you draw from those funds.

While 25% of most pensions can usually be taken tax-free, the remaining withdrawals are subject to Income Tax.

This means you need to be aware of higher tax thresholds and ensure that you keep your income within lower tax bands as far as possible.

You should also look ahead to see how frozen tax thresholds could affect you in future years. The effect of these could be that more of your income becomes taxable, even if your spending has not increased.

With planning, you can identify these risks early and adapt your income strategy accordingly.

Effective Inheritance Tax planning can help you secure your legacy

In addition to planning your income, your tax planning strategy in retirement should address the legacy you leave to your beneficiaries.

Once you have retired, estate planning becomes increasingly important, as you’ll start to get a clear idea of the assets that will form that legacy and the possible implications for your family in terms of the Inheritance Tax (IHT) they may be liable for after you pass on.

There are various strategies you can put in place to reduce the potential IHT liability on your estate. These include gifting assets, making regular gifts from your surplus income, using life insurance, and using trusts.

All of these strategies involve careful planning. The earlier you consider them, the more flexibility you will have to structure your affairs in a tax-efficient way.

You should regularly review your plans

It’s almost inevitable that your financial circumstances will change during your retirement. Because of that, the income and tax planning strategies you put in place when you first retire may not be suitable later on.

For example, you may receive an inheritance or sell a property – both of which will provide you with a capital sum to factor into your planning.

Closer to home, you may suffer a deterioration in your health or experience changing family circumstances that will necessitate amendments to your plans.

Additionally, external factors, such as legislative changes, could affect your planning. We have certainly seen this in recent years with changes brought in the Budget.

Regular reviews of your financial situation can help you make informed decisions and ensure your strategy remains aligned with current tax legislation and your evolving needs.

Expert advice can help you stay on track

As you may now appreciate, retirement tax planning can be a complex process, especially if your income is derived from multiple sources.

Decisions around how and when to withdraw funds can affect your tax liability to a significant degree, and any mistakes can easily impact your long-term financial security.

By working with an expert, you can identify tax-efficient strategies, reduce unnecessary liabilities, and ensure your retirement income is structured effectively.

You should also bear in mind that your plans will need to adapt to your changing financial circumstances.

Get in touch

If you would like to discuss your retirement income and tax planning, please get in touch.

You can call me on 07769 156250.

Please note

This blog is for information purposes only and does not constitute advice or a personalised recommendation. The information is aimed at individuals only.

Please do not act based on anything you might read in this article. This blog is based on our understanding of current and proposed legislation, which may change.

The value of your investments (and any income from them) can go down as well as up, and you may not get back the full amount you invested. Past performance is not a guide to future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

When investing, your capital may be at risk.