Thinking backwards: A different way to plan your retirement

Most people plan their retirement by looking forward, trying to envisage their perfect future. “What do I want to do? Where do I want to live?” Unfortunately, most people have no idea what they want.

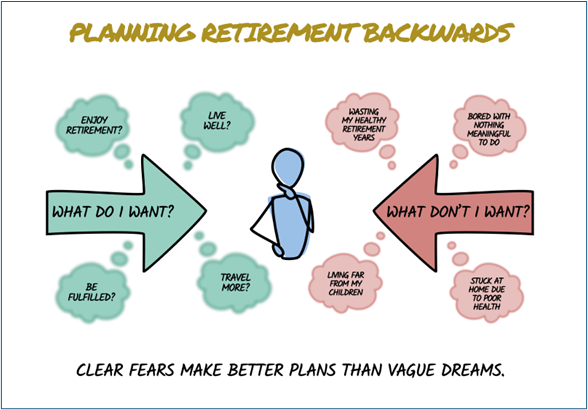

Ask someone to describe their ideal retirement and you’ll get vague answers. “Travel more.” “Spend time with my family.” These sound nice, but they’re not specific enough for planning.

Here’s a different approach that gets you better answers much faster: start with what you don’t want. This comes from Charlie Munger, who made “invert, always invert” one of his core principles. Instead of asking “How do I succeed?”, consider asking “How do I fail?” and then work to avoid those outcomes.

When you ask “What would make my retirement miserable?”, the answers come quickly. These fears are specific and actionable.

So, avoiding them brings you remarkably close to the life you want.

4 overlooked mistakes you need to avoid

The financial regrets of retirement get all the attention. Not saving enough, retiring too early, and underestimating costs are common financial pitfalls.

I believe four lifestyle mistakes can ruin your retirement, even if you believe you have a secure income in place.

1. Missing your active window

Most people have roughly 15 years of healthy, mobile retirement before things get harder. Yet, many waste these precious years because they didn’t plan for travel and adventure while they could still enjoy them.

2. Losing your identity and purpose

After 40 years of career structure, many retirees feel completely lost. They have money, but it lacks a sense of usefulness or meaning. The days feel empty because work provided more than just income.

3. Relationship isolation

Some retirees find themselves living far from adult children and grandchildren, or they’ve let friendships fade during busy career years. Money can’t buy back lost time with people you love.

4. Neglecting your health in your 50s and 60s

This is when prevention matters most. Poor health choices during these years can significantly reduce the quality of your entire retirement, regardless of how much money you have saved.

All these issues can be avoided entirely through proper planning.

Applying inversion thinking to your retirement planning

While most people do post-mortems after something goes wrong, a “pre-mortem” imagines failure before it happens. It’s simpler than it sounds.

Begin by imagining you’re 80 years old, reflecting on your retirement with profound regret. Ask yourself: “What went wrong?”.

What do you wish you’d done differently? Don’t overthink this. Your gut reactions are usually the most telling. Write down everything that comes to mind, no matter how obvious it seems.

Next, get specific. Instead of “I wish I’d travelled more”, ask “Where exactly did I want to go, and when was the best time to do it?”. Instead of “I should have stayed healthier”, ask “What specific health habits would have made the biggest difference?”.

Then, work backwards to today. For each regret, identify what you need to start doing now to prevent it. If your biggest fear is losing touch with your children, consider where you’ll live in retirement. If you’re worried about losing your sense of purpose, consider developing interests beyond work.

The goal isn’t to solve everything today. It’s about gaining clarity on what matters to you, so you can begin incorporating those elements into your plan. This exercise may take 30 minutes, but it can save you decades of regret.

Harness the power of inversion thinking

Most retirement advice focuses on the numbers. How much to save, when to retire, how to invest. These are important, but they’re not enough.

The retirement that will bring you fulfilment requires thinking beyond the spreadsheet. It requires imagining not just the money you’ll have, but the life you’ll live with it.

Inversion thinking gives you a practical way to do this. The pre-mortem exercise we described isn’t a one-time activity. Your fears and priorities will change as you get closer to retirement. What feels important at 50 might look different at 60. Regular check-ins help you stay on track.

The financial aspects of retirement are well understood. Do the work now to avoid the lifestyle regrets later. If you’d like help applying this thinking to your specific situation, I’m always here to guide you through the process.

Get in touch

If you would like to talk about your own retirement plans, or any of the issues raised in this article, please get in touch.

You can call me on 07769 156 250.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.