Who wants to live forever? How longevity can impact your retirement planning

I’ve just read a book called The 100-Year Life by Lynda Gratton and Andrew Scott.

It explains how increased longevity is changing our lives – and will continue to change them in the future.

It then considers how we will have to adapt different aspects of our lives to cope with this in order to be able to embrace a long life as a gift, rather than as a curse.

It set me thinking about how increased longevity can impact on financial planning, particularly when it comes to retirement.

We’re living longer than our parents

Life expectancy is rising. People retiring now are likely to be spending far longer in retirement than their parents and grandparents.

According to the Office for National Statistics, a 67-year-old male has an average life expectancy of 85 years. For a 67-year-old female, the average life expectancy is 87.

Bear in mind those are average figures. This means that the man has a 25% chance of reaching 92. The woman has the same chance of living to age 94.

Reinforcing the fact that we’re living longer, some fascinating research published at the turn of this century revealed some startling statistics. Over the last 200 years, life expectancy has expanded at a rate of more than two years every decade. This means that:

- If you are now 20, you have more than a 50% chance of living to 100

- If you are 40, you have an even chance of reaching 95

- If you are 60, then you have a 50% chance of making it to 90 or older.

This clearly poses a challenge when it comes to financial planning for your retirement.

Why we’re living longer

To realise why we’re living longer, you just need to consider the differences in lifestyle between today and previous generations.

There have been spectacular advances in healthcare provision meaning that health threats, such as some forms of cancer, that would previously have been fatal are now survivable. The standard of primary care has also come on in leaps and bounds. The big reduction in the number of people who smoke is evidence of how effective health education can be.

Pharmaceutical companies can also react quickly to threats to our health and wellbeing. The toll from the Covid-19 virus has been sobering, but consider how many lives would have been lost and how we’d have had to change our lifestyles had a vaccine not been developed so promptly.

Increased longevity creates problems when it comes to financial planning

Increased longevity is clearly a positive development. Living longer means you get to spend more time with loved ones and have longer to do the things you dreamed of while you were working.

However, it also raises other issues.

It’s understandable if you have concerns about the quality of your life as you get older. Certain, previously fatal illnesses may no longer limit your lifespan, but they can still incapacitate you and mean you’re dependent on others.

This can impact on your family if you can be looked after in your own home. It can also affect your finances if you require long-term care.

Longevity can also pose challenges when it comes to your retirement income planning.

One simple life-stage outline I’ve heard advisers use in the past is the “20-40-20” rule. This means that after 20 years of childhood and education, you work for 40 years, and then have 20 years of retirement.

Changing working patterns, and the increase in longevity we’ve already covered, means that the last two parts of that three-part life journey have become increasingly fluid.

This makes planning for retirement even more challenging.

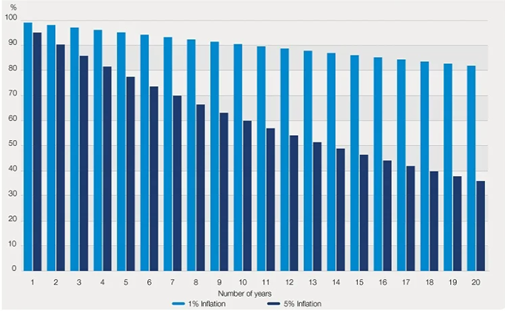

Inflation is the hidden threat to your financial wellbeing

Another issue related to longevity that, to my mind, doesn’t get talked about enough, is the impact of inflation.

Putting it bluntly, if you’re living longer, inflation has more time to have a potentially devastating impact on the value of your income in retirement.

This table shows the impact of inflation rates of 1% and 5% over a 20-year period.

Source: Schroders

For example, if you started taking an income of £20,000 when you retired at age 66, an annual inflation rate of 5% would mean that this would be worth less than £8,000 in real terms by the time you reached 86.

Apart from your State Pension, you’re unlikely to have any “new” money coming into your retirement fund after you retire.

Investment growth can be a counterweight to the impact of inflation. This makes it all the more important that you have an effective investment strategy in place.

How longevity impacts on your financial planning

When it comes to planning for your retirement, the first step should always be to start putting a plan together.

Two key questions you should consider as part of your planning process are:

- How much money will I need to live on in retirement?

- When do I want to stop working?

The answers to those questions lead on to a third:

- What changes do I need to make to my lifestyle and finances?

Clearly, no one knows how long they will live for. If we did, financial planning would certainly be more straightforward – although life would very unsettling and would potentially resemble a sci-fi film.

Uncertainty makes financial planning more difficult in the first place, but also more important; the less that’s left to chance, the better. The key challenge is making sure your money outlives you and not the other way around!

Life expectancy should be a key part of your financial planning process. How much you save and how you invest your retirement fund are key issues.

As you’ll have seen from the chart earlier, the ever-present threat of inflation makes those issues even more important as you plan your future.

Get in touch

I can’t tell you how long you’re going to live, but I can help you put a financial plan together to give you the best possible chance that you won’t outlive your money.

To find out more, please give me a call on 07769 156 250.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Foster Denovo Limited is authorised and regulated by the Financial Conduct Authority.

The Financial Conduct Authority does not regulate school fees planning, taxation & Trust advice and Will writing.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.