How to protect your retirement income from inflation

For many years, high inflation has been treated like a historical relic from the 70s and 80s that no one was worried about anymore.

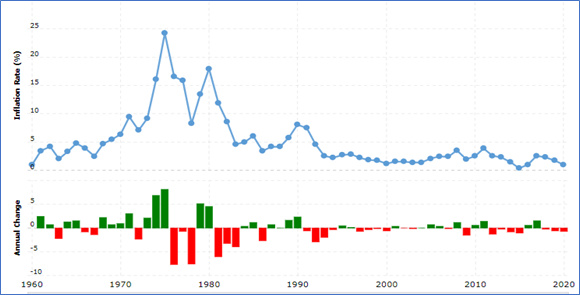

A quick glimpse at this chart shows the relative stability we’ve enjoyed for the best part of three decades. In fact, we’ve probably enjoyed the longest run of sustained low inflation since the period between the defeat of Napoleon in 1815 and the start of World War I.

Annual inflation rates from 1960 to 2020. Source – Macrotrends.net

Yet memories of high inflation as the nemesis of many government and individual financial plans are strong in many people’s minds – which explains the recent concerns around rising inflation as global economies emerge from lockdown.

In June 2021, UK inflation was 2.5% – the highest figure for three years.

Although experts disagree over whether this is a short-term threat or the start of a whole new and financially dangerous epoch, there’s no doubt that it should be a big consideration when planning your financial future.

Much like that other own 70’s relic – the shark in Jaws – inflation can be a silent killer when it comes to your retirement income.

Read on to discover how inflation can impact on your retirement plans, and some key steps you can take to protect yourself against it.

Inflation reduces the value of your savings

In simple terms, inflation erodes the purchasing power of your cash.

For example, if you go shopping today, £100 will currently buy you £100 worth of goods. But if annual inflation is 5%, in a year’s time those goods will cost you £105. This means you’ll either need to find another £5 from somewhere or be frugal and buy £5 less of goods.

In the short term, that will just about work. However, over a longer period, if your income isn’t going up and you’re only getting a derisory interest rate on your savings, it’ll start becoming a problem.

Over the 30-year period we mentioned previously, inflation has pushed prices up by more than 80%, but the average savings account return is less than a quarter of that.

While you’re working, the problem of inflation will likely be alleviated by “cost of living” increases to your salary, as well as the usual process of you earning more the longer you work.

However, once you stop working, and start living on your pension and other savings, inflation becomes a very real issue.

You need to invest your money to beat inflation

Ideally the value of your pension fund needs to keep track, or preferably exceed, the rate of inflation. As you aren’t earning new money, this will ensure you can draw enough money to maintain your standard of living without having to take too much from your fund.

The State Pension and most final salary schemes generate an income that is designed to provide an element of inflation-proofing. But what about your capital?

Your investment strategy, therefore, becomes all-important. If you can achieve and maintain investment growth that exceeds the rate of inflation, you can put yourself in a far more secure position than if you’re just holding your money in cash.

Historically, stock markets have done a great job of delivering investors with returns above inflation. For example, over the last 10 years, the MSCI World Index has grown at an average of 11.66% each year in US dollar terms to 30 July 2021 and provided inflation-beating returns.

A suitable investment strategy is crucial

A certain amount of investment acumen is required when it comes to putting a robust portfolio together, because some sectors are likely to be a better option than others.

For example, rising prices, and therefore increased costs, could have a detrimental impact on manufacturing businesses, and hit their profitability.

On the plus side, however, commodity share values tend to go up when inflation is at higher levels.

Probably the key factor to bear in mind is that the steps taken to achieve a higher expected return will generally mean having to accept a higher level of investment risk. This will almost inevitably result in price fluctuation as greater exposure to the stock market means exposure to market volatility.

Remember you’re investing for the long term, and that study after study has shown that long-term stock market equity investment will typically outperform inflation.

According to data from Trustnet, over the last 10 years the annualised performance of the FTSE 100 has been 7.5%. That compares very favourably with CPI over the same period, which has averaged just 1.8% annually.

Hedging part of your portfolio against inflation

It’s likely that you will have an element of your investment portfolio set aside to provide you with a secure income in the event of any sudden market downturn – such as that we saw at the start of the Covid pandemic in 2020. Here, inflation linked bonds (ILB) could be an option.

ILBs are specifically designed to protect investors from the impact of inflation. They will be issued by the UK government and their performance will be linked to the consumer price index. The value will therefore rise in line with inflation, but not exceed it.

Get in touch

High inflation, resulting in continuing rising prices, can impact on even the most carefully laid out retirement plans by reducing your purchasing power.

I can help you adapt your investment strategy – reducing levels of fixed-income investments and focusing more on higher growth opportunities – to mitigate the impact of inflation and ensure your retirement income strategy stays on course.

To find out more, please give me a call on 07769 156 250.

Please note

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Foster Denovo Limited is authorised and regulated by the Financial Conduct Authority.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

This article is for information purposes only and does not constitute advice or a personalised recommendation.